It was a year when crude oil got crushed, when shares of the world's biggest tech company – and its much smaller Canadian rival – made a comeback. It was also the year when the formerly high-flying loonie went for a swim, Stephen Harper's favourite coffee and doughnut chain ended up in the jaws of a burger joint and investors got high on drug stocks. Even as markets rose, however, some companies with outsized dividends took an axe to their payments, and not just in the oil patch.

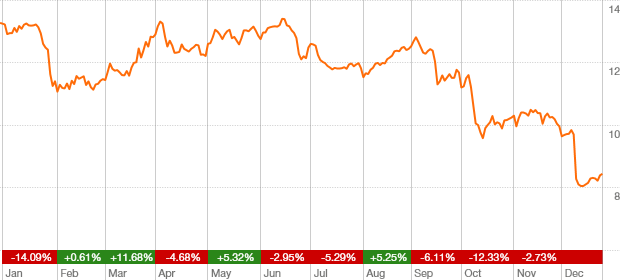

Crude Oil - West Texas

WTI (CL-FT)

Dec. 26, 2014 settle: $54.73 (U.S.)

down $43.97 or 44% over year

Various theories have been advanced to explain the dramatic drop in the price of crude oil: The Saudis and Americans are teaming up to destroy Vladimir Putin; The Saudis are trying to kill the U.S. shale energy industry; Slowing global growth has led to a glut of oil. We prefer a simpler explanation: More sellers than buyers. Whatever the cause, crude oil’s swift decline cut a swath of destruction through Canada’s oil patch, sending stocks to multi-year lows and prompting energy producers to slash dividends and scale back capital spending plans, while stoking worries about the sustainability of government budgets that depend on oil and gas tax revenues. Of course, lower oil prices have some beneficiaries, too - airlines, cruise ship operators and SUV dealers, for example. Unfortunately, the planet isn’t one of them.

Canadian dollar

CAD

Dec. 24, 2014 close: 86.04¢ (U.S.)

down 8¢ or 8.5% over year

It wasn’t long ago that Canada held itself in great financial and economic esteem, our banking system a bastion of financial prudence in world awash in risky lending, our economy, stock market and currency all reflective of the Canada’s elevated post-crisis standing within the G8. But there’s nothing quite like a crash in oil prices to expose Canadian weaknesses. The energy selloff has cast a pall over the Canadian economic outlook, dragging the Canadian dollar down to within two-fifths of a penny, at one point in mid-December, of crisis-era lows more than five years ago. Through the year, the loonie declined by about 8 cents against the U.S. dollar, which is newly invigorated from signs of a resurging economy. Going into 2015, the currency slide has juggled Canadian fortunes both by sector, with exporters and manufacturers suddenly more competitive, and by geography, with Ontario and Quebec poised for growth and Alberta set to decline.

Avigilon

AVO (TSX)

Dec. 24, 2014 close: $17.25

down $13.50 or 44% over year

This former tech darling, which makes high-definition surveillance equipment, could use a little of its patented clarity at the corporate level. At the start of the year, Avigilon was coming off of two years in which its stock rose by 190 per cent and 160 per cent respectively. Its market value topped $1-billion in late 2013, earning Avigilon inclusion in the S&P/TSX composite index, before the stock was derailed by investor speculation. First there was a string of management departures, including the company’s CFO, who left the day before first-quarter earnings were released. Suspecting something was wrong within the company, investors sold the stock down by 30 per cent over one week. In July, Veritas Investment Research detailed a number of concerns with the company’s financial reporting, including changing auditors twice in the last five years and changing how the company records revenue. There’s no “smoking gun,” Veritas said, but for investors, there was more than enough smoke. They were further encouraged to sell by earnings volatility, and the stock ended the year on a 44-per-cent decline.

AGF Management

AGF.B (TSX)

Dec. 24, 2014 close: $8.44

down $4.83 or 36% over year

With an outsized yield of 11 per cent and a business that’s been shrinking for years, AGF was perhaps the most obvious candidate for a dividend cut since that other infamous yield trap, Yellow Pages Income Fund. But investors still took it hard when the struggling fund company chopped its payout, slicing it to 8 cents a quarter from 27 cents - down 70 per cent. As if that wasn’t punishment enough, the shares promptly suffered their biggest one-day rout on record, making investors that much poorer. AGF is vowing to reinvest the cash to turn its business around, but with its investment products underperforming and banks increasingly dominating the fund landscape, analysts warned that AGF’s struggles are far from over: even after the dividend cut, more than 80 per cent have a ”hold” or “sell” rating on the stock.

Just Energy

JE (TSX)

Dec. 24, 2014 close: $6.03

down $1.57 or 21% over year

As an investment, Just Energy has been just awful. Since trading for more than $15 in 2011, shares of the door-to-door gas and electricity marketer - infamous for its high-pressure sales tactics - have shed about 60 per cent of their value. What’s more, the cash investors counted on from the stock has also been dropping fast: Weighed down by debt and faced with growing competition, the company slashed its dividend twice - a 32-per-cent reduction in 2013, followed by a 40-per-cent cut in 2014. Just Energy is trying to strengthen its balance sheet by selling off non-core assets - in November it closed the sale of its National Energy rental water and HVAC business for $505-million - but given the company’s dismal track record, winning back the faith of investors - and consumers - will be no small challenge.

Tim Hortons

THI (TSX)

Dec. 12, 2014 close: $98.00

up $36.01 or 58% over year

Great Canadian assets that slipped into foreign hands:

1) Gretzky traded to the Kings;

2) Mark Carney hired away by the Bank of England;

3) Tim Hortons gobbled up by Burger King.

Apart from the obvious operational synergies of combining a doughnut and burger chain – volume discounts on hair nets, for example – the highly leveraged merger’s main advantage for BK’s Brazilian owner is Canada’s lower tax rate. If you believe the press releases, on the other hand, it’s all about taking the iconic Tim Hortons brand around the world where people who have never watched hockey or rolled up the rim will suddenly embrace the company’s mediocre coffee and baked goods. Well, we can think of at least one jurisdiction where that might be true: North Korea’s Kim Jong Un looks like he would enjoy the occasional family pack of Timbits.

Note: THI's final day of trading was Dec. 12. For current stock activity, see Restaurant Brands Int'l (QSR-T) the parent of Tim Hortons and Burger King.

Amaya

AYA (TSX)

Dec. 24, 2014 close: $28.20

up $20.25 or 255% over year

Owning stock in Amaya this year was not unlike a visit to an underground poker room – daring bets, accusations of cheating, and the chance that the coppers would bust down the door, flip the tables, and tell everyone to scram, see. The Quebec-based online gambling company jolted the industry in June with a highly leveraged $4.9-billion (U.S.) acquisition of the company that owns the PokerStars and Full Tilt Poker sites. While those two sites claim up to two-thirds of the online poker market, they have been effectively shut out of the U.S. since a Department of Justice crackdown in 2011. The Amaya deal, with the backing of Wall Street investment banking powerhouse Blackstone Group, was supposed to lend a measure of corporate legitimacy to the sites’ effort to re-enter the U.S. Then in mid-December, investors learned of an investigation by the Quebec securities regulator into trading activity surrounding the acquisition. But the 20-per-cent share price drop that followed didn’t threaten the stock’s position atop the S&P/TSX composite index’s rankings, with a 255-per-cent rise on the year, proving a good bet for Amaya’s shareholders with the stomach to let it ride.

BlackBerry

BB (TSX)

Dec. 24, 2014 close: $12.41

up $4.51 or 57% over year

Like the BlackBerry faithful still pounding out emails on battered Bold handsets, the company’s stock has a contingent of devoted investors convinced of a return to glory. They’ve endured years of slights from the likes of Apple investors for clinging to an outdated tech stock in comparison to Apple shares, which gleam with modernity and teem with value. BlackBerry CEO John Chen rewarded both users and investors for their loyalty this year, the former with the launch of the Classic smartphone – a throwback to the CrackBerry era, and the latter with the relatively successful completion of the turnaround’s first phase. While revenues continue to decline, producing much volatility in share price, the company ended the year on a relative high note, with the goal of positive cash flow reached a quarter earlier than promised, and the stock marking a 57-per-cent gain, placing it among the top ten on the S&P/TSX composite index.

Allergan

AGN (NYSE)

Dec. 26, 2014 close: $211.95 (U.S.)

up $100.87 or 91% over year

Valeant Pharmaceuticals and its shareholders suffered through a furrow and frown-inducing failure to acquire Allergan, but the Botox maker came out the big winner in rebuffing the advances of the Canadian suitor. Valeant spent more than half the year in pursuit of a deal that could have made it the biggest company in Canada by market capitalization. Things turned nasty when Valeant started a proxy fight and tried to replace the board with directors friendly to the deal. And even though the acquisitive Canadian company twice raised its offer, Allergan preferred the affections of white knight Actavis PLC in a deal valued at $66-billion (U.S.). Through what was one of the biggest global M&A deals of the year, Allergan’s stock increased by 90 per cent on the year. The company’s investors should avoid excessive smiling, however, lest the fine lines set in.

Apple

AAPL (Nasdaq)

Dec. 26, 2014 close: $113.99 (U.S.)

up $33.84 or 42% over year

Not long ago, investing in Apple was about as much fun as tripping on the curb and dropping your new iPhone down a sewer grate. From a high of more than $100 (U.S.) in 2012 (adjusted for this year’s 7-for-1 split), the shares plunged to less than $56 in 2013, hammered by growing competition from Samsung, glitches with the iPhone’s mapping software and a dearth of blockbuster new products. In the post Steve Jobs era, Apple seemed to have lost its way. Well, surprise: The stock has regained all the ground it lost and then some. Helped by the recent launch of larger-screened iPhones and slimmer and faster iPads, Apple’s market value in November briefly topped $700-billion - a first for any company. Some analysts are predicting that Apple is on its way to becoming the first $1-trillion company - if the gains don’t evaporate like they did last time, that is.